At the end of November, the European Commission published the Bioeconomy Strategy, updating the initial strategy published in 2012 and revised multiple times over the last decade. With a total value of €2.7 trillion in 2023 alone, the EU’s bioeconomy represents an extraordinary driver of European competitiveness, alongside the Union’s ambition to reach and stick to its climate goals.

The Bioeconomy Strategy is indeed one of the main pillars of the Clean Industrial Deal announced by the Commission almost one year ago. It goes to the heart of the dilemma that has been -picking Brussels’ minds in recent months: how to combine economic competitiveness and industrial development with environmental protection.

What is the bioeconomy?

According to the Commission’s definition, the bioeconomy comprises “the activities that deliver sustainable solutions based on biological resources to create added value.” These activities involve a wide range of products, services and technologies, which emcompasssectors such as agriculture, food, health, energy, industry, ecosystems and other related services.

The overarching goal of the European Bioeconomy Strategy is to promote sustainability, resource efficiency and innovation, leveraging the EU’s knowledge, nature and biological resources to reduce dependence on fossil fuels, mitigate climate change and support circular business models. This includes managing natural resources responsibly and transforming waste into value.

Fit for neutrality: the EU’s long-term vision for 2040

The Strategy aims to indicate a clear way forward to build a sustainable bioeconomy. It intends to do so by:

- Scaling up investments and innovation

- Building new markets for bio-based materials and technologies

- Ensuring a sustainable biomass supply

- Harnessing and fully exploiting global opportunities

In the Commission’s vision for 2040, Europe should have widely deployed and fully leveraged sustainable bio-based materials and products such as construction materials, biochemicals, textiles, fertilisers, plant protection products and plastics.

Their advantage lies not only in providing an alternative to fossil-based products, but also in significantly contributing to Europe’s economic growth, jobs and incomes. Studies have shown that over the last ten years the bioeconomy sectors in the EU have grown faster than the overall economy, representing a key opportunity for future clean growth in the decades to come.

The main challenges and opportunities ahead

1. Regulatory complexity and market fragmentation

One of the main challenges for the effective and timely deployment of bio-based products is regulatory complexity. This stems not only from uncertainty on how to classify and categorise novel solutions but is further aggravated by diverging national rules among Member States.

This overall complexity results in market fragmentation, which increases the cost of doing business, especially for SMEs. For this reason, one of the starting points of the Strategy is to simplify regulatory requirements while, at the same time, accelerating permitting and authorisation procedures for these products to be placed on the Single Market.

The Commission plans to address this in a second step with the publication of two “Biotech Acts”:

- a first one on health, expected by the end of 2025

- a second one covering agriculture, food, energy and environment, to be unveiled in the third quarter of 2026

As anticipated by the Commission, the Biotech Acts will introduce sectoral and horizontal enablers such as fast-track authorisation procedures for microbial and other biotechnological solutions for industrial use , while streamlining permitting.

In this sense, SMEs should engage in Brussels to help shape the drafting of these key legislative proposals and ensure their voice is heard, particularly on simplifying regulatory burdens and accelerating permitting procedures. At Lykke Advice, we specialise in providing SMEs with tailored support to convey their priorities and concerns to EU policymakers and stakeholders, who are increasingly keen to listen to, and reflect in legislation, the perspectives of the smaller business community.

Relevant competent agencies, such as the European Food Safety Authority (EFSA), the European Chemicals Agency (ECHA) and the European Medicines Agency (EMA), will cooperate more closely and in a more coordinated manner to speed up authorisation and verification procedures. The aim is to ensure that these products can enter the market more easily, while safeguarding safety and maintaining high standards.

To support SMEs in scaling up and developing bioproducts, the Commission has also announced the use of regulatory sandboxes. These will allow companies to test new products and services in real-world environments without being immediately subject to the full regulatory burden. This approach enables innovation while preserving consumer protection and market integrity.

For SMEs, these sandboxes are not just a technical tool, but a concrete opportunity. They make it possible to test innovative technologies in dialogue with regulators, reduce the time and cost of bringing products to market, and obtain early feedback on how future rules will be designed and interpreted. By operating in a controlled environment, SMEs can demonstrate the safety and performance of their solutions, de-risk their business model in the eyes of investors and lenders, and build a much stronger case when applying for EU or national funding. In practice, however, many SMEs lack the time and in-house regulatory expertise to identify relevant sandboxes, understand eligibility criteria and translate technical results into convincing policy messages. This is precisely where specialised public affairs support in Brussels, such as that offered by Lykke Advice, can help SMEs secure access to these instruments and make sure that their experience feeds directly into the design of future EU rules.

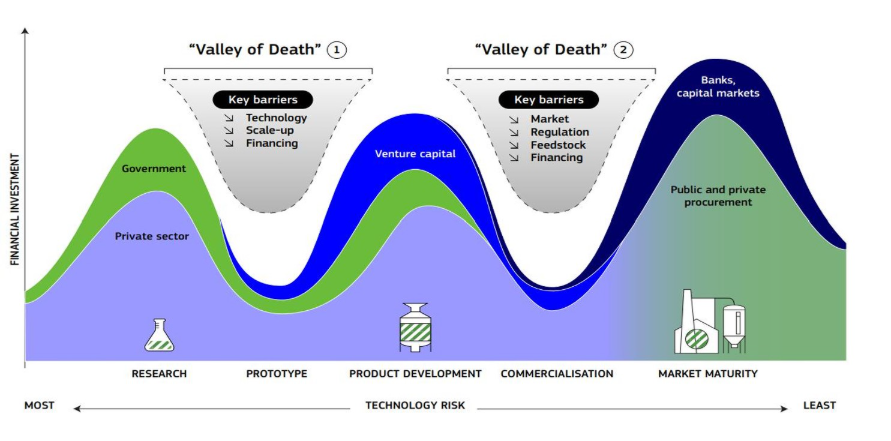

2. The investment gap and the “two valleys of death”

A second major challenge the sector is facing is the investment gap. According to a report published by the European Investment Bank (EIB) last year, the EU needs to invest an additional €350 billion per year to meet its sustainability targets under the Green Deal. However, the specific share destined to the bioeconomy remained unclear until now.

By aggregating the investment needs across different bioeconomy sectors, including agriculture, irrigation, agri-food, bio-based industry, bioenergy, fisheries and natural resource protection, the EIB has estimated an annual investment gap of €121.8 billion in the EU.

The Life Sciences Strategy and the EU Start-up and Scale-up Strategy, recently released, aim to provide the framework to accelerate innovation, improve market access and scale up new technologies. However, the Commission itself acknowledges the need to complement these strategies with sector-specific targeted investments, paying special attention to tailored financing solutions for SMEs.

The EIB has been one of the main lenders to the bioeconomy, contributing around €7 billion a year to co-finance projects in agriculture and the bioeconomy. A significant proportion of this financing (around 65–70%) goes to SMEs via intermediated financial products, principally loans provided by the EIB to local banks, which are then used to offer advantageous financing for specific policy objectives.

In addition, in recent years the EIB has supported the bioeconomy through Cohesion Funds, the European Agricultural Fund for Rural Development (EAFRD), Horizon Europe and InnovFin. Nonetheless, the financing gap remains far from being closed, and companies still struggle to escape the so-called two “valleys of death” in the scaling up of the bioeconomy in Europe.

Source: European Commission

- The first valley of death occurs during the research and development phase, when technologies must prove their technical and economic viability. In this phase, private investors, by nature risk-averse, are often reluctant to invest, leading to an overall decline in investments.

- The second valley of death arises in the commercialisation phase, when companies seek to scale up industrial production. Here, key barriers relate to market access, regulation and financing.

Public investment should therefore be protected and reinforced to help bridge these two valleys by compensating market failures and keeping investment ratios high.

The Commission states that its proposal for the next Multiannual Financial Framework (MFF) will increase funding for the bioeconomy through the European Competitiveness Fund (a €200 billion fund) and the Horizon Europe programme. However, it remains unclear how this will be implemented in practice, especially given the lack of clarity on on which areas and how the money from the Competitiveness Fund will be spent.

In fact, the European Parliament has voiced growing criticism in recent months regarding the Commission’s decision to merge programmes for health, biotech, defence and other key sectors into a single instrument, raising concerns about transparency, prioritisation and effectiveness.

A positive element, on the other hand, is the initiative launched by the Strategy to work with Member States to align national investment priorities in the bioeconomy and to support the sector through more Important Projects of Common European Interest (IPCEIs).

Taken together, these challenges are real and should not be underestimated. However, the new Bioeconomy Strategy also creates a unique window of opportunity for SMEs. By signalling clear political support for bio-based solutions, identifying priority value chains and mobilising new funding instruments, the EU is effectively saying that it wants more innovation from smaller players, not less. The question is no longer whether bio-based business models will grow, but who will define the standards, shape the regulatory benchmarks and capture the first-mover advantage. SMEs that engage now stand a much better chance of influencing this emerging framework and positioning themselves as indispensable partners in its implementation.

By being active in Brussels, SMEs will have the opportunity to closely monitor and meaningfully influence the negotiations on the next Multiannual Financial Framework, helping to shape the Commission’s political priorities for the seven-year EU budget. Representation in Brussels also opens a privileged channel with the European Investment Bank and other managing authorities of EU funding instruments, enabling SMEs to better access EU funds to test, scale up and further develop their bio-based products and services.

The key sectors for the bioeconomy in Europe

To unlock private investment and venture capital, the Strategy seeks to identify markets where bio-based solutions can deliver high added value and where they are sufficiently mature to achieve ambitious and tangible results. Efficient use of biomass will help the EU reach its net-zero goals under the Green Deal and create added value, positioning Europe as a global leader in exporting these innovations.

In 2022, biomass in the EU was primarily used for:

- Animal feed (38%)

- Energy (29%)

- Materials (24%)

- Food (9%)

While bio-based materials often struggle to reach economies of scale due to higher costs and low demand, there are some markets where bio-based solutions have the potential to overcome these barriers and attract investment to scale up in the coming decades. These include:

- Bioplastics, biopolymers and bio-based fibres for packaging

These products offer a clear alternative to fossil-based plastics in the packaging sector and in industrial applications, by providing a lower carbon footprint, reducing external dependence on fossil resources and enabling new applications for biodegradable bioplastics.

Under the already adopted Packaging and Packaging Waste Regulation, the EU will support the uptake of bioplastics and novel materials, as well as set recycled content targets for these materials.

- Textiles from bio-based fibres and fabrics

Textiles also have a crucial role in the Commission’s thinking for the coming years. Work is ongoing on the revision of Product Environmental Footprint (PEF) methods, which will include indicators to help consumers understand the benefits of materials such as bio-based textiles.

Additionally, under the Ecodesign for Sustainable Products Regulation (ESPR), the Commission will set durability requirements for textiles, including those made from bio-based fibres.

- Bio-based chemicals derived from renewable biological sources

In this area, the Commission intends to support the development of solutions that provide alternatives to conventional chemical substances. With the revision of the REACH Regulation still pending and not expected before March–April 2026 (according to the latest indications), the Commission aims to back the scale-up of industrial biotechnology for the production of bio-based chemicals.

- Bio-based construction products

The construction sector is responsible for roughly 35% of total EU waste generation and 5–12% of total EU greenhouse gas emissions. The Commission sees in bio-based construction products, such as wood and fibre-based materials, a major opportunity to reduce embodied carbon and energy demand, while increasing carbon storage in buildings.

The Strategy recognises the crucial role played by long-lasting biogenic carbon storage in recent years and announces a methodology to include it within the scope of the Carbon Removal and Carbon Farming Certification Framework. In other words, bio-based solutions are key not only to reducing emissions, but also to capturing, storing and reusing the carbon already present in the environment.

- Bio-based fertilisers and plant protection products

The Strategy foresees an important role for bio-based fertilisers and plant protection products, which can lower import dependence and reduce carbon footprints by turning agricultural residues and local organic waste into value-added inputs.

On this specific point, the Strategy is particularly right to underline the huge potential of bio-based solutions in turning waste into value, by transforming and reusing bio-based by-products in economic activities.

Reducingthe carbon footprint

The Strategy is ambitious in aiming not only to reduce the carbon footprint of new products, but also to cut existing carbon in the atmosphere and in soils. With new biotechnologies, CO₂ and carbon captured from the atmosphere and from soils can be effectively transformed into energy and heat. It is indeed good news that in the Strategy the Commission recognises bioenergy as continuing to play a role in energy security, particularly where it uses residues, does not increase water and air pollution, and complements other renewable sources.

In the same vein, the Commission signals an important, if still modest, step by announcing its intention to explore, in the context of the revision of the EU Emissions Trading System, possible pathways to recognise biogenic permanent removals as certified under the Carbon Removal and Carbon Farming Framework.

Implementation and the way forward

Now that the Commission has finally acknowledged the central contribution of bioeconomy technologies, recognised the challenges and set out a roadmap to scale up investment and innovation, the focus will inevitably shift to implementation, where a real qualitative leap is needed.

The Commission will soon unveil the first Biotech Act for the medical sector, while the second Biotech Act, covering other technologies, is expected in the third quarter of 2026. These will be accompanied by another crucial pillar that will complement the Strategy and boost implementation: the Circular Economy Act.

Given the broad range of competences involved, the revision of the Common Agricultural Policy (CAP) will also play a crucial role in supporting bio-based proteins and materials for agri-food production. Meanwhile, the Energy Grids Package and the Electrification Action Plan will be important additions on the energy side, helping to integrate bio-based solutions into a modern, flexible and decarbonised energy system, while the Soil Monitoring Law and the Deforestation Regulation will complement the frame on land and forestry use.

Why SMEs should engage now

For all these reasons, the new Bioeconomy Strategy is a major opportunity. SMEs operating in the bio-based solutions space, or using innovative bio-based technologies, are often closest to the market and quickest to experiment. If they engage early in Brussels, they can help ensure that the upcoming legislative proposals reflect technological reality and create a regulatory environment that rewards innovation rather than punishing it.

The implementation of the Strategy and the drafting of the Biotech Acts, the Circular Economy Act and other forthcoming initiatives will directly shape the business models, compliance costs and access to finance of bio-based SMEs. Being present and active in Brussels will enable them to help set policy priorities, influence how rules are interpreted and implemented, anticipate regulatory changes instead of reacting to them, seize emerging funding opportunities, build a strong business case for their products and services, attract investors and partners, and ultimately scale up in a way that is both competitive and sustainable.

The Bioeconomy Strategy sets the political direction; it is now up to policymakers, investors and innovators, particularly SMEs, to provide EU institutions with input from the ground and ensure that this vision turns into concrete projects, jobs and value along the whole bio-based value chain. Lykke Advice is a Brussels-based public affairs consultancy whose primary mission is to help SMEs make their voice and interests heard by EU institutions and key stakeholders. By offering tailor-made support on advocacy, funding and strategic positioning, we help smaller businesses navigate the EU policy process with confidence and turn the opportunities created by the Bioeconomy Strategy into tangible growth.